Seeds of Gulf-Africa agribusiness

When Gulf nations face food, security, and water scarcity issues, one response is to seek lucrative agricultural investments in fertile African lands. Yet, while such deals can bring benefits to the countries involved, there are also sizeable risks

By Sarah Townsend

Soaring temperatures, sun-baked earth, and dwindling water supplies: the Arabian Gulf’s blistering hot summer this year was, for many, a stark reminder of the impact of global warming on the fast-growing desert region. In June, Kuwait and Saudi Arabia recorded the highest temperatures on Earth for this year: 52 and 55 degrees Celsius, respectively. This was all precluded by warnings from meteorologists, including from a team at the Massachusetts Institute of Technology in 2015, that future temperatures in the Gulf could exceed the threshold for human survival if nations do not reduce carbon emissions.

The inhospitable summer was also a reminder of the pressures the region faces on its food and water supply. The wider Middle East and North Africa (MENA) region has less than 2 percent of the world’s renewable water supply, and water availability is six times less than the worldwide average, according to the World Bank. MENA countries cannot sustainably meet current water demands, and the World Bank predicts that that water availability per capita will halve by 2050 due to climate change and population growth.

In the six-member economic bloc of the Gulf Cooperation Council (GCC)— comprising the United Arab Emirates, Saudi Arabia, Kuwait, Qatar, Bahrain, and Oman—food resource pressures are particularly acute. The International Monetary Fund projects the GCC’s population will grow by an average of 2.4 percent annually in the next five years to reach 57 million by 2025. As a result, regional food consumption is set to expand at an annual rate of 3.3 percent between 2018 and 2023, according to the Dubai-based investment bank Alpen Capital.

Yet, the prospect of growing crops on such arid land to feed the hungry is slim. World Bank figures show that the GCC has among the lowest proportion of arable land in the world, ranging from 0.2 percent of the total land area in Oman to 2.1 percent in Bahrain. This compares to above 30 percent for many European countries and above 40 percent for some countries in Africa.

The combination of desert climate, water scarcity, and limited arable land to grow crops has resulted in a high dependency on food imports, exposing Gulf economies to global food price fluctuations and trade fallouts from geopolitical conflict. GCC imports are projected to double between 2009 and 2020 to reach $53.1 billion, according to research from The Economist. The economic blockade of Qatar by Saudi Arabia and its allies since 2017, and ongoing tensions with Iran, are compounding uncertainty.

Gulf nations are ultimately facing a food security crisis—and are now actively looking outside their own borders to secure future food supplies. Less-developed countries with vast swathes of uncultivated arable land in Africa, central Asia, and other regions are among the main targets for investment by the oil-rich GCC.

Last October, Abu Dhabi hosted the second international Agriscape conference, aimed at stimulating agricultural investments abroad. The country wants to ramp up its involvement in global “agribusiness,” the term used to describe farming for commercial purposes and the numerous trades that support agricultural production. These include crop production, processing and distribution, sale and distribution of farm machinery, livestock breeding, agrichemicals and marketing, and retail and sales operations.

During Agriscape, the United Arab Emirates (UAE) food security minister, Mariam Hareb Almheiri, made a bold proclamation of the country’s ambitions, stating, “As food security is a pressing resource security challenge for the UAE, we have a keen interest in increasing agricultural efficiency through the adoption of new methods and diversifying the pattern of agricultural investment abroad…to support sustainable development and bridge the nutritional gap.”

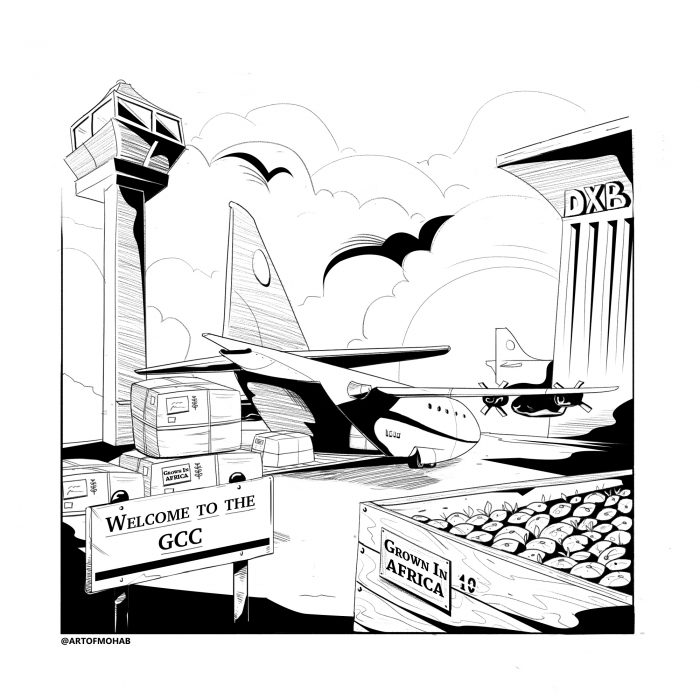

Africa’s Link in the Gulf Food Chain

Some five thousand kilometers south of Abu Dhabi in Zambia, a plane operated by the cargo division of Dubai’s flag carrier Emirates takes flight, loaded with crops, seeds, and other agricultural exports bound for the Gulf. A property valuer who specializes in farm sales and asked to remain anonymous said representatives of Gulf royal families, sovereign wealth funds, and other investors from the region have sought agricultural investments in the landlocked southern African country. The volume of enquiries has risen substantially since last year’s Agriscape, the person added.

In Zambia, Gulf investors are mainly looking at outright acquisitions of farms and farmland worth two hundred million British pounds and above, with a focus on grains, sugar, beans, and seed production, as well as dairy and goat farming. “They want to produce it here, take it to the Gulf, and then store it for twenty years or more to boost food security,” the valuer explained, adding that many of the wealthiest investors seek discretion above all, and usually strike deals via local “fixers”. These fixers organize indirect investments through special purpose vehicles, which are organizations that invest indirectly through funds or other legal entities.

The UAE, which imports about 90 percent of its food, was one of Zambia’s top export destinations in 2017, accounting for $313 million, according to figures from the Observatory of Economic Complexity. Total non-oil trade between Africa and the UAE stood at $24 billion in 2016, up from $17.5 billion in 2014, according to the Dubai Chamber of Commerce.

Saudi Arabia is another GCC country with agricultural interests in Zambia. In 2011, the Arab kingdom’s Manafea Holding unveiled plans to invest $125 million in developing a five-thousand-hectare farm in Zambia’s Northwestern Province to grow pineapples and other fruit for export to Saudi Arabia. Manafea also pledged to build two thousand housing units for farm staff near the capital city of Lusaka. The project was expected to create employment opportunities for local communities and connect small-scale farmers to the larger Africa–Gulf market through distribution contracts.

Saudi Arabia also has invested heavily in Ethiopian agriculture through companies such as Saudi Star Agricultural Development, which in 2011 committed to invest $2.5 billion in agribusiness in the East African country by 2020. The firm pledged to develop a rice farm in the Gambella region on ten thousand hectares of land leased for sixty years, and rent a further 290,000 hectares.

The kingdom also has sizeable interests in Sudan and elsewhere in Africa as part of the King Abdullah Initiative for Saudi Agricultural Investment Abroad, which launched in 2009 in an attempt to encourage Saudis to buy land overseas and help overcome food and water shortages in the kingdom. Other examples of Africa–Gulf agribusiness deals include last year’s pledge by Hassad Food, a subsidiary of the gas-rich Gulf state Qatar’s sovereign investment fund, the Qatar Investment Authority, to invest $500 million in Sudan’s agricultural and food sectors over three years.

Meanwhile, the UAE launched a potentially groundbreaking proposal to invest in African agriculture last October when it signed a deal with Uganda to establish one of the world’s first agricultural free zones in the East African state. Under the plan, the 2,500-hectare free zone will allow companies from the UAE to invest in agricultural production and development in Uganda and export produce to the UAE on favorable trade terms. If it comes to fruition, the project could stimulate commercial farming activities in Africa and protect the UAE’s food supply chain for years to come.

There are fewer publicized examples of Gulf agricultural investment in North Africa. However, increasing political and economic stability in Egypt, and measures introduced by the Moroccan and Egyptian governments to incentivize foreign investment, are making these countries more attractive.

In 2018, Morocco’s agricultural output rose by 60 percent to exceed $13 billion after the 2008 launch of the government’s Green Morocco Plan. The initiative aimed to increase farm income from the limited swathes of fertile land in the mountainous country through the adoption of new irrigation and other farming technologies to boost output and lower costs. At the SIAL Middle East industry expo in 2015, the UAE pledged investments totalling $41 million in projects to grow olives, citrus, red fruit, and other produce in Morocco.

Tunisia is another North African country that is attracting greater attention from Gulf investors as it looks to accelerate economic growth following a period of political and national insecurity following the Arab Spring in 2011. Where there is the right investment framework and political stability, GCC investors may find it easier to strike deals in Muslim-majority North Africa due to cultural and linguistic ties and physical proximity.

Measuring the Potential of African Farmlands

There are two things to note. First, it is difficult to gauge with certainty the extent and value of Gulf agribusiness in Africa because many of the investments are indirect, making it hard to identify the stakeholders. The website Landmatrix. org goes some way toward identifying Gulf land deals in Africa; however, not all are documented.

Second, Africa is not the only continent to which the GCC is looking in order to shore up its food supply. Gulf states are also making investments in Europe, Central Asia, the United States, and more established farming markets such as Argentina and Brazil, where global investors have held farming interests for many decades. In Africa, the Gulf faces intense competition with Chinese investors, who are increasingly striking huge deals to support farming through the provision of new infrastructure built by Chinese contractors. This can mean Gulf investors have to work harder to beat the competition and strike favorable deals, or look to other farming markets where there is less competition, to ensure food security.

Some GCC countries are even attempting to stimulate agribusiness at home through national farming initiatives. The UAE has begun investing in agricultural-technology (“agri-tech”) firms. These firms are developing innovative farming techniques to overcome the barriers of water scarcity and barren soil. Abu Dhabi this year launched a $350 million scheme to help establish agricultural technology companies in the emirate.

Perhaps more strikingly, oil-rich Qatar is building a series of dairy farms in the desert and wants to become self-sufficient in milk production. When the Saudi-led air, land, and sea blockade began to threaten the flow of Qatari imports, the authorities set out to boost domestic agricultural production by airlifting four thousand cows into the desert and embarking on a strategy to develop up to 1,400 farms across forty-five thousand acres of land by 2022—no mean feat for a country with less than eighty millimeters of rainfall per year. According to the UK-based trade newspaper Dairy Reporter, the cows live in huge air-conditioned sheds at a farm approximately fifty-five kilometres from the Qatari capital city of Doha. The herd is expanding in line with the farm’s target of owning twenty-four thousand cows within the next decade, and produces a reported 320 tons of milk each day, which is processed using European equipment to boost output.

Notwithstanding these points, there are clear reasons why African agribusiness appeals to Gulf investors. The World Bank estimates that Africa has around 60 percent of the world’s uncultivated arable land and uses only 2 percent of its renewable water resources compared to the global average of 5 percent.

Yet, political and economic instability in some countries has hampered the cost-effective use of that land and the efficient distribution of produce from it. Post-harvest losses are between 15-20 percent for cereals and higher for perishable products due to poor storage and limited farm infrastructure, the World Bank says.

As such, Africa remains a net importer of food despite its obvious potential, while hunger and malnourishment remain a critical issue. Africa’s population is set to nearly double to 2.5 billion by 2050, according to the United Nations, and agriculture will be key to feeding and employing people. The World Bank says Africa’s food market, which was valued at around $303 billion in 2010, could triple to reach nearly $1 trillion by 2030 as investments in trade, technology, and infrastructure link farmers with bigger markets and higher quality land.

When seen in this context, rising Gulf interest in Africa is unsurprising. The latest Near East and North Africa Regional Overview of Food Security and Nutrition report, published this year by the Food and Agriculture Organization of the United Nations, lays bare the extent of food insecurity in the Gulf. The population-weighted average prevalence of “severe” food insecurity in the population between 2015 and 2017 stood at 7.6 percent for GCC countries— higher than the weighted average of 1.3 percent for developing nations, but still well short of developed nations’ 10.8 percent, the report said.

Unsurprisingly, GCC leaders speak less of this and more of the financial reward—which has the potential to be great. “Only 5 percent of African land has been utilized for agriculture and many of the consumers are coming from Africa. Imagine if we find a way to tap into that,” Khadim Al Darei, deputy chairman of UAE-based agribusiness firm Al Dahra, told Agriscape.

For the Gulf, African agribusiness is not only an answer to a pressing food security question, but also an exciting commercial prospect. The UAE was the second largest investor country in Africa across all sectors in 2016, with a capital investment of $11 billion, according to fDi Intelligence—showing the scale of regional interest in the continent.

Deal or No Deal? Barriers to Investing in African Agribusiness

By partnering with farmers in joint ventures, acquiring land outright, or otherwise investing in African farmlands, the Gulf can ensure a sustainable food supply while boosting African economies: a win-win for the parties involved. However, it is not all that straightforward. Above and beyond the quality of land, the success of a venture depends on how a deal is structured to benefit landowner, community, and investor, and the policies and legal frameworks put in place to enable this economic relationship to occur.

Some African countries have well-considered regulations to help attract foreign investors, while ensuring local people retain a stake. For example, to invest in Moroccan farming, it is necessary to partner with a local company or individual who will own a proportion of the venture. Unfortunately, in many other countries, “the agriculture industry is not terribly well organized,” says Willem Janssen, lead agricultural economist at the World Bank. “This means that the response of investors—including those from the Gulf—is to broker a deal that allows them almost full control of the operation. For example, they will buy up one thousand hectares of land and develop a self-sufficient system around it, to cultivate land and export the produce.”

There are big dangers if the local community is not involved in the project—for instance, if it does not employ local workers or if some of the produce does not find its way into the hands of the surrounding villages and towns. King Abdullah’s overseas farming policy led to riots and killings in Ethiopia in 2012, when hostile locals unleashed deep grievances on Saudi Star’s Gambella farm. A group of gunmen, reported at the time to have been Anuak militants, opened fire at the compound and killed at least five employees before fleeing. Reprisals followed and, according to Human Rights Watch, the military rounded up villagers, beat the men, and raped the women.

This is the dark side of what critics term the African “land grab”—an unsettling economic imperialism where affluent countries use their deep pockets to impose industrial-scale farming practices on what were traditional smallholdings from which local people made a living.

Saudi Star is still operating in Ethiopia, but armed guards around the farm’s perimeter are a reminder of previous unrest. The story demonstrates the potential for negative social, political, and economic ramifications in Gulf– Africa agribusiness. African nations are growing rapidly, yet affluent nations are seeking arrangements with them to produce, distribute, and appropriate their most valuable resource: food. Because of this, potential investors have to understand that cross-regional deals impose practical and ethical responsibilities on the countries involved. Stakeholders should work to balance conflicting interests and manage the impact of outside powers to ensure adequate protection of African food supplies and mitigate the risk of causing injustice and disquiet.

It is no coincidence that in the past years, many of the biggest foreign agricultural projects have been in countries racked by political and social instability—for example Sudan, the Democratic Republic of Congo, and Ethiopia—where governance procedures to ensure local people benefitted from foreign investment were flimsy or non-existent. For a long time, it was easy for investors to take a bite of the land without giving back. Or, if they did have to give back, it was through an illicit payment to corrupt governments. However, things are changing for the better, as governments strengthen their governance systems and realize how economically vital it is to compete with other countries for valuable foreign investment.

Still, there are other hurdles to cross. In Africa, the cost of land is cheap, but farming is labor and knowledge-intensive and requires supporting infrastructure to be commercially viable. Economist Janssen likens it to the running of a safari lodge. The nightly rate is high, but such operations rarely make a profit because they are typically located hundreds of kilometers from the nearest road or town and it costs a fortune to transport guests, food, and other supplies to and from the lodge.

In Tanzania, the government has created a new capital city, Dodoma, in the heart of the country. The land is not well developed or well connected, so the authorities have had to construct roads and infrastructure so the city can function. Similarly, an average ten to fifteen-thousand-hectare farm requires a workforce of around five hundred people to work the land. With their husbands, wives, and children you suddenly have a community of three to four thousand to accommodate, which requires the building of a school, clinic, church, and recreational facilities. None of this comes cheap, and investors must build all of this into their plans. By contrast, much of the farmland in developed markets such as Argentina and the United States has infrastructure in place and it is easier “to just step in,” Janssen explains.

Toward a More Efficient Export System

The final missing piece for investors is their ability to export produce without constraints within a fair and open trading regime. This is where many African countries are falling short. Trade policies tend to be highly politicized. If there are national food shortages, food is not allowed to leave the country. Granting exclusive rights to foreign investors rarely works, because everybody comes in and requests special treatment. As a result, many Gulf investors head to countries that are better organized. However, there are possible solutions on the horizon. The creation of dedicated agricultural free zones such as the proposal from the UAE and Uganda is one, because it overcomes the problem of having to develop infrastructure around arable land. For Uganda, which has high levels of debt (forecast to rise to almost 50 percent of GDP by 2020–21), the free zone is an opportunity to secure fresh foreign capital to plug its deficit. For the UAE, Uganda could offer an export licence to new businesses to incentivize them to set up shop there.

Another way to energize Afro–Gulf economic links is through the African Continental Free Trade Agreement, signed last year. It aims to create a “single continental market for goods and services, with free movement of business persons and investments,” according to the African Union. The sheer size and the fractured nature of intra-African trade has hindered countries’ abilities to trade with one another, thereby hampering the flow of foreign investment across the continent, and internationally.

“Helping Africa realize its trading potential could…open a new agricultural market for Gulf states to exploit,” said a 2018 report by Australian not-for-profit Future Directions International. Gulf–Africa agribusiness is a clear opportunity for all parties involved, but it must be innovative, fair, and carefully handled in order to be sustainable. Care must be taken that land acquisitions and leases are priced correctly and do not threaten people’s livelihoods, and that robust trade and infrastructure frameworks are put in place.

One of the most important principles in business is that of the risk-return trade-off. The greater the level of risk an investor is willing to take, the greater the potential return—and this is certainly true of farming ventures in Africa. If Gulf investors hit the jackpot in Africa, they can do extremely well, but there is also a high potential for it all to go wrong.

There is a pressing need to maximize output from one of the world’s most fertile continents and increase food security for both GCC and African nations. The parties involved have clear incentives to make this work. With the right approach, the arid Arabian Gulf can develop Africa’s bountiful lands to feed their own people, while helping partner countries prosper for decades to come.

Sarah Townsend is an award-winning business and public policy journalist who worked in the Middle East for five years, including at the UAE’s biggest English language daily, The National, and Gulf current affairs magazine Arabian Business. In 2017, she won the CFA Institute’s Financial Journalist of the Year (EMEA) award. On Twitter: @SP_Townsend.