TIAA’s farmland funds linked to fires, conflicts and legacy deforestation risks in Brazil

This report analyses the sustainability and financial risks of the farmland investment funds of the Teachers Insurance and Annuity Association of America (TIAA, formerly TIAA-CREF) in Brazil. Such risks are most prevalent in Matopiba, Brazil’s newest soy frontier, consisting of part of the states of Maranhão, Tocantins, Piauí and Bahia. TIAA farmland investments operate through various companies, such as Radar and its subsidiaries, that acquire and manage properties. CRR’s sustainability analysis shows that deforestation and fires have taken place on TIAA’s farmland portfolio, enabling negative social impacts on local communities.

Download the PDF here: TIAA’s Farmland Funds Linked to Fires, Conflicts and Legacy Deforestation Risks in Brazil

Key Findings:

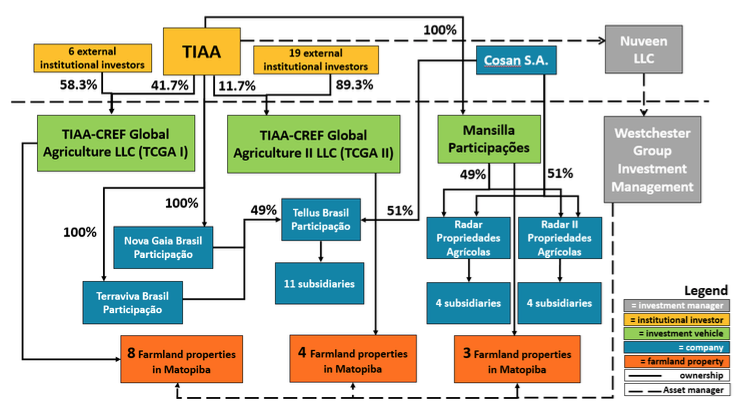

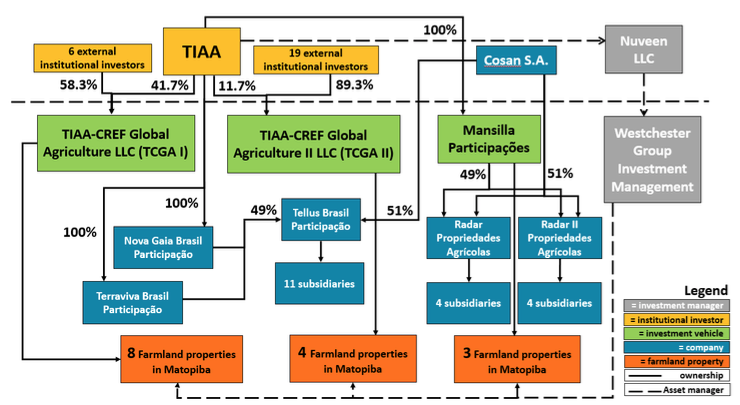

Radar is part of a complex web of companies through which TIAA invests in Brazilian farmland assets. TIAA has been accused of using complicated corporate structures to circumvent legal restrictions on foreign land ownership. Farmland acquisitions are funded through investment vehicles financed by 20 different institutional investors.

Despite a recent increase in transparency, the land portfolio in TIAA’s investment vehicles remains unclear. TIAA’s asset manager, Nuveen, maintains a public map with farmland holdings. However, Nuveen’s information does not fully match public ownership records.

Between 2009 and 2018, a total of 2,970 ha were cleared on six TIAA portfolio farms in Matopiba. In August 2019, fires burned 2,350 ha on three farms. While pre-2018 deforestation is not in violation of Nuveen’s zero-deforestation policy, Nuveen may not be able to sell properties with post-2009 clearing to any counterparty with a similar or stricter zero-deforestation policy.

Radar properties may be linked to land-grabbing and conflicts with local communities in Matopiba. At least 22,834 ha on six of Radar’s properties were bought from companies linked to Euclides de Carli. The Brazilian Public Prosecutors Ministry is investigating De Carli’s land acquisitions and has suspended the titles of 124,000 ha in Piauí and Maranhão.

Value loss in Radar’s portfolio in Matopiba could amount to USD 192 million. Although this amount represents 23 percent of Radar’s assets, the loss would total only 0.6 percent of Nuveen’s global farmland fund and portfolio and 0.07 percent of Cosan’s enterprise value.

The lack of transparency may put investors in conflict with their climate change policies and lead to reputation risks. Lenders include BNP Paribas, Santander, Rabobank and HSBC; farmland fund participants with policies include AP2, Caisse de depot and ABP.

Radar is part of TIAA’s complex web of Brazilian farmland investment companies

Radar Propriedades Agrícolas (Radar) is a Brazilian company established in 2008. Radar was founded as a joint venture between Cosan and Mansilla Participações, with initial capital of USD 400 million. Cosan, a Brazilian company, is active in the energy and logistic sectors. It has a joint venture with Shell (Raízen, from 2011) for production and distribution of sugar and ethanol, and owns ComGás, a subsidiary for the distribution of natural gas in Brazil. Mansilla is a wholly-owned subsidiary of the Teachers Insurance and Annuity Association of America – College Retirement Equities Fund (TIAA, formerly TIAA-CREF).

In October 2016, Cosan sold an undisclosed share of Radar to Mansilla for BRL 1.06 billion (USD 326 million). As a result, Mansilla holds 100 percent of Radar’s preferred shares, while Cosan maintains most of its ordinary shares. Although TIAA maintains 97 percent of Radar’s capital, Cosan still controls Radar under Brazilian Law.

Radar is part of a complex web of companies through which TIAA invests in global farmland assets. Radar is an intermediary company structured to comply with Brazilian land ownership law. Brazilian Law limits foreign ownership to 25 percent of a municipality’s area. Until 2010, companies jointly owned or managed by Brazilian and foreign entities were considered to be Brazilian. These companies were not held to municipality ownership restrictions. However, in 2010, the Brazilian General Counsel’s position paper, accepted by the President, proposed that mixed companies (controlled by national and international entities) should be considered foreign companies, limiting their land acquisition operations.

TIAA has been accused of using complex corporate structures to obscure foreign ownership of land acquisition entities and circumvent these new legal restrictions. After the 2010 regulatory restrictions on land acquisition by mixed companies, Cosan and TIAA established Tellus Brasil Participações (Tellus) specifically for land acquisition (see Figure 1). Through several subsidiaries, such as Terra Viva Brasil Participações and Nova Gaia Brasil Participações, Tellus is 51 percent owned by Cosan and 49 percent by TIAA, and thus considered a mixed company. Tellus raises funds for farmland purchases through debentures to Radar and other subsidiaries. According to TIAA’s quarterly statement, more than 20 different companies are listed under indirect or direct ownership and/or management of Radar and Tellus in Brazil. These companies cover operations linked to capital gathering, land acquisition, and the clearing, preparing, leasing, and selling of properties. In 2012, Radar obtained an additional tax ID number to form Radar I and Radar II.

A new bill under consideration in the Brazilian Senate proposes to facilitate foreign investments in land acquisitions in Brazil. In May 2019, Senators proposed a new bill for alterations on Article 190 of the Federal Constitution. The proposal calls for the inversion of the 2010 rule. It would recognize companies with mixed capital or management between Brazilian and foreign companies as Brazilian. The proposal also increases the limited area that foreign companies can own per municipality’s territory, likely further opening Brazil to international investments seeking economic development.

Figure 1: Radar and Tellus ownership structure

Source: CRR based on TIAA Quarterly Statement (June 2019) and Rede Report on Radar

Farmland investments are a key alternative investment strategy

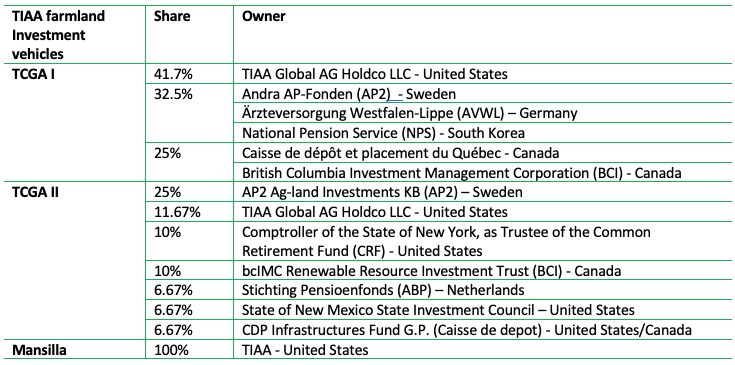

TIAA’s asset manager Nuveen has USD 1 trillion assets under management. It considers farmland investments an important pillar of its alternative (USD 97 billion assets under management) investment strategy. In 2011, TIAA launched its first Global Agriculture Fund (TCGA I), raising USD 2 billion from institutional investors (see Figure 2). In 2015, it launched TCGA II, raising an additional USD 3 billion. Nuveen has unified all farmland asset management under a single firm, Westchester Group Investment Management. With funds from TCGA I, TCGA II, and Mansilla, Westchester controls farmland assets in the United States, Australia, Brazil and Chile. The Brazilian entities Radar, Tellus and affiliated entities are all managed by the Westchester Group.

Figure 2: Institutional investors with a 5 percent or higher stake in TIAA affiliated farmland investment vehicles

* Source: SEC Form N-4 Filing (December 2016)

Radar’s land holdings lack transparency

Despite recent efforts to increase transparency, Radar’s and its associated companies’ land portfolio remains unclear. Nuveen maintains a public online map with farmland holdings to provide “transparency in how we pursue sustainable practices through our investments globally.” However, Nuveen’s information on its website does not fully match public ownership records.

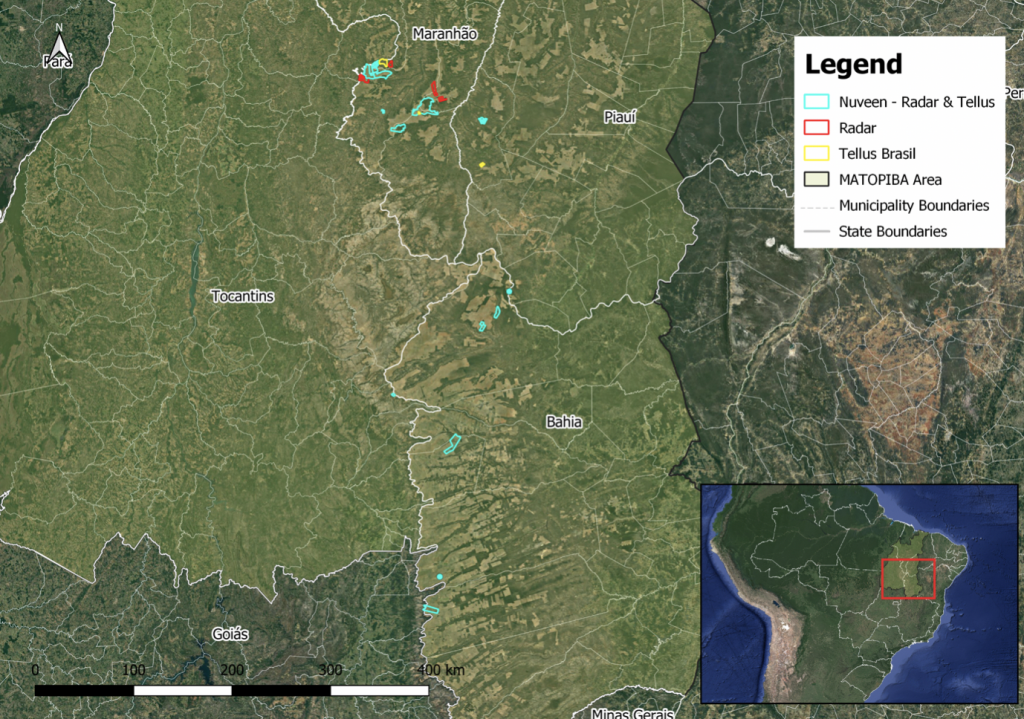

Nuveen’s publicly available farmland map lists 58 properties in Brazil, of which 15 are in Matopiba. The map lists the tillable area (77,271 ha for the 15 properties in Matopiba) for each farm but does not provide the exact boundaries. Ownership records from the Instituto Nacional de Colonização e Reforma Agrária (INCRA) suggest that Radar and affiliated companies are the registered owners of a total of 111,703 ha of land.

The discrepancy between Nuveen’s reporting and public ownership records are the result of differences in the tillable reported area of farms and the public ownership registration of these farms, as well as unreported properties. According to INCRA’s records, the total area of the 15 reported farms is 95,067 ha. In Nuveen’s portfolio, eight of these farms are linked to TCGA I; four to TCGA II; and three to Mansilla (see Figure 3).

Figure 3: TIAA’s reported farmland portfolio in Matopiba (Brazil)

Elaborated by CRR in partnership with REDE Social de Justiça e Direitos Humanos. Sources: Nuveen(*) and INCRA(**). All the owners’ companies are listed in the TIAA-CREF Quarterly Statement (September 2019) and the “no info” status means that it was not possible to confirm the ownership of the land.

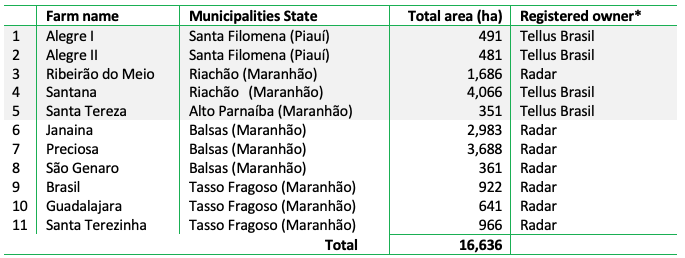

Fieldwork and INCRA records also revealed an additional 11 properties in Matopiba with a total area of 16,636 ha linked to Radar and its affiliated companies (see Figure 4 and 5). These properties are not listed on Nuveen’s farmland map. Radar informed CRR that the entire area of five of these farms is registered as Legal Reserves of other properties listed in its public portfolio (marked in grey in Figure 3), following the Brazilian Forest Code. The other six farms found by CRR were, according to Radar, part of other properties listed in its public portfolio (Figure 3).

Figure 4: Radar’s and Tellus’ farms in Matopiba region of the Cerrado biome (Brazil)

Elaborated by CRR in partnership with REDE Social de Justiça e Direitos Humanos. Sources: fieldwork and INCRA.

Figure 5: Radar’s farms location in Matopiba, Cerrado biome (Brazil)

Elaborated by CRR in partnership with REDE Social de Justiça e Direitos Humanos. Sources: fieldwork and INCRA.

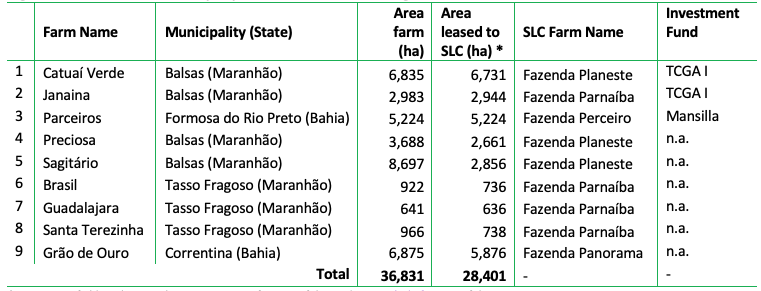

Within Radar’s portfolio, CRR found nine properties entirely or partially leased to SLC Agrícola (Figure 6). Leasing farms to SLC Agrícola in Matopiba is part of Radar’s strategy for increasing the value of the land before selling it and sending the profits to investors who are part of its TCGA’s investment funds. SLC Agrícola does not have a zero-deforestation policy.

Figure 6: Radar and Tellus properties leased to SLC Agrícola

*Source: CRR field work in October 2019, Nuveen farm portfolio, and SLC Agrícola farm portfolio.

Nuveen is the first farmland investor with a zero-deforestation policy

Nuveen has a zero-deforestation policy for its farmland investments in Brazil. The policy, adopted in August 2018, prohibits new purchases of farmland cleared of native vegetation after predefined cut-off dates. The cut-off dates correspond to the most relevant deforestation protocols for Brazil’s various biomes, including the Soy Moratorium, the Grãos Verdes Protocol, and the UN Convention to Combat Desertification. For the Cerrado biome, the date is May 2009 or later in accordance with criteria set forth by the Roundtable for Responsible Soy (RTRS). Nuveen’s sustainability report of 2019 includes a recent ESG audit developed by independent organizations covering 30 percent of its properties in Brazil (approximately 101,000 ha out of a total of 338,654 ha). However, the report does not specify where the audited farms are and if the audit covered its portfolio in the Matopiba region of Cerrado biome.

Nuveen’s zero-deforestation policy does not specify any commitments for farms already in its portfolio.

Nuveen informed CRR that land acquisition and native vegetation clearing between May 2009 and June 2016 in the Cerrado biome was in accordance with criteria put forth by the Round Table on Responsible Soy (RTRS) (Brazilian revised version). Nuveen also indicated to CRR that “properties acquired before and after this date [August 2018] can’t under any circumstances be converted.”

Nuveen informed CRR that land acquisition and native vegetation clearing between May 2009 and June 2016 in the Cerrado biome was in accordance with criteria put forth by the Round Table on Responsible Soy (RTRS) (Brazilian revised version). Nuveen also indicated to CRR that “properties acquired before and after this date [August 2018] can’t under any circumstances be converted.”

Catuaí Norte, a 17,825-ha farm in Balsas, Maranhão, provides an example of Nuveen’s compliance of its zero-deforestation policy. Catuaí Norte is part of TCGA I (see Figure 2) and purchased by Westchester Group in 2013. 38 percent of the Catuaí Norte farm is registered as the mandatory Legal Reserve under the Brazilian Forest Code, although 45 percent is covered by native vegetation. The report says that Catuaí Norte has an “extra preserved vegetation area” of about 1,219 ha (around 7 percent of its total area) in addition to the Legal Reserve requested by law. Nuveen’s 2019 sustainability report also affirms that conservation of this “extra preserved vegetation area” is an example of compliance with the objectives of its zero-deforestation policy, as this area could be legally converted into cropland.

2,970 ha of post-2009 deforestation may result in legacy compensation liabilities

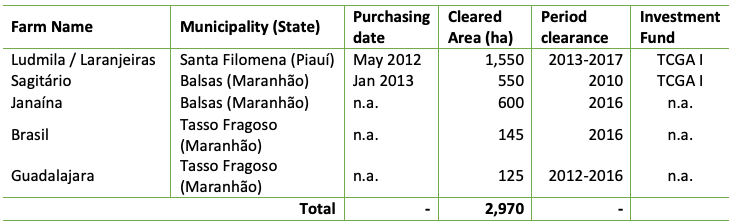

Between 2009 and 2018, a total of 2,970 ha were cleared on five Radar or Tellus farms in Matopiba (see Figure 7). Since these farms were already part of Radar’s portfolio in August 2018, the clearing does not violate the letter of Nuveen’s zero-deforestation policy. No deforestation was detected after the adoption of the policy in August 2018. However, deforestation between May 2009 and July 2018 took place on two farms that were in Radar’s possession at the time of the clearing. On one farm, deforestation happened prior to Radar’s investment. For three farms, the exact acquisition date could not be determined.

Figure 7: Post-2009 deforestation on Radar’s farms in Matopiba region of Cerrado biome

Source: PRODES

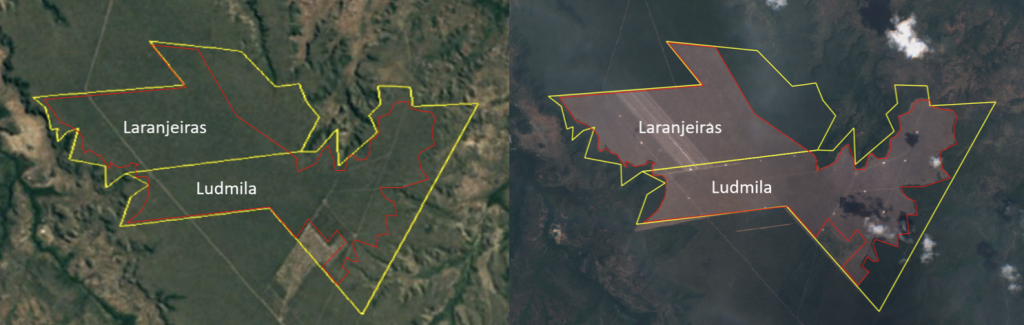

The Laranjeiras and Ludmila farms in Piauí saw 1,550 ha of native vegetation clearance after Radar’s acquisition in May 2012 (See figure 8). Radar indicated to CRR that all the native vegetation clearance in Laranjeiras and Ludmila farm were part of its agriculture expansion plan. The Legal Reserve of the Ludmila and Laranjeiras farms is partially within the property and partially in two remote locations registered as Alegre I and Alegre II (see Figure 9). Radar considers the four farms to be one property. Registration of Legal Reserves in remote properties is regulated according to the Brazilian Forest Code and by the Piauí Forest Law. Radar said that the Legal Reserve is 1,324 ha, when considering the total area of the four farms as one property (Ludmila, Laranjeiras, Alegre I and Alegre II). Although the compensation of Legal Reserves in other properties is allowed by Law, some discussion currently focuses on its inefficiency in guaranteeing local environmental services. Large areas nearby without native vegetation contribute to short-term local impacts on biodiversity, water sources, soil nutrition and rainfall. These impacts increase also the risks of agribusiness operations in the Cerrado biome.

In fieldwork CRR conducted in partnership with REDE Social de Justiça e Direitos Humanos in 2019, local communities reported impacts linked to the Ludmila and Laranjeiras farms in Santa Filomena, Piauí. The communities close to the Laranjeiras and Ludmila farms reported violent episodes involving people who used to work with the previous owners of both farms. These conflicts started in 2010 and accelerated in 2015, which included burning of local communities’ houses and plantations. Radar declared that, based on its visit to the area in 2017, it did not find any conflict between the operations within both farms and local communities. CRR’s fieldwork also showed that Tellus Brasil, the owner of Ludmila farm, requested to split its subdivision into three different properties (the farms Piqui, Frutal and Limoeira). It is not clear if this subdivision is linked to selling or leasing plans, which Radar has not confirmed. Local communities reported the clearance of native vegetation happening on the Ludmila farm in 2018, which CRR was not able to confirm through satellite images. However, CRR visually confirmed that native vegetation clearance on this farm happened mostly in 2013. Radar reported that it started agriculture operations on this farm on 2018. The area was most likely abandoned between 2013 and 2018, the period in which native vegetation started to regenerate. In 2018, local communities reported that Radar’s operations led to deforestation.

Figure 8: Deforestation in Ludmila and Laranjeiras farms in Santa Filomena, Piauí, in Matopiba between 2013 and 2017

Elaborated by CRR. Imagery by Google Earth and Sentinel-2 image

Figure 9: Registered Legal Reserves and Permanent Preservation Areas of Ludmila, Laranjeiras, Alegre I and Alegre II farms in Santa Filomena, Piauí

Elaborated by CRR. Imagery by Google Earth and Sentinel-2 image. Sources: INCRA and Serviço Florestal Brasileiro

Recent fire events on Radar’s properties in Matopiba

Recently, the massive fire events in Brazil received widespread international attention. The Amazon fire events that started in August 2019 were the largest since 2010 and an increase of almost 80 percent compared to August 2018. At the same time, fire events also increased in the Cerrado, which registered more fire alerts than the Amazon in August 2019. The fires in the Cerrado and the Amazon between August and September 2019 were mostly caused by human activity and were exacerbated due to the dry season. Particularly in the Cerrado, the increase of fires has also been a direct consequence of deforestation, which is already causing higher temperatures during dry seasons and worsening fire events. Fires are also a direct consequence of deforestation, which is already causing higher temperatures during dry seasons and in turn worsening fire events.

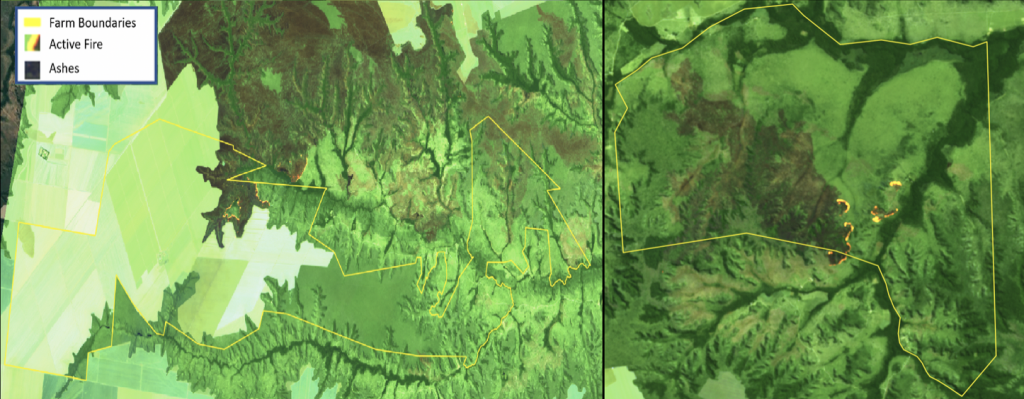

In August 2019, fires burned an area of 2,350 ha on three Radar farms. A recent report by GRAIN highlighted fire events on Harvard University and TIAA farms in Matopiba. Considering only the properties on which CRR found more than five fire alerts, fire events between August and September 2019 took place on seven different farms owned by Radar, Tellus, and its subsidiaries in Matopiba. CRR confirmed fire events on three of these farms in Maranhão: 870 ha in Santana (Riachão), 750 ha in Catuaí Norte (Alto Parnaíba), and 730 hectares in Sagitário (Balsas), the last leased to SLC Agrícola (see Figure 10 and 11).

Figure 10: Nasa fires alerts from August to September 2019 in Radar’s farms in Matopiba

Source: National Aeronautics and Space Administration (NASA).

Around 66 fire alerts from August and September 2019 were detected on the Catuaí Norte farm in Balsas, Maranhão. CRR visually confirmed that these fire events resulted in the burning of at least 750 ha within the Legal Reserve of the farm. Nuveen uses the Catuaí Norte farm as an example of how it preserves native vegetation in an area larger than what is mandated by the Brazilian Forest Code. Nuveen informed CRR that the fire events in Catuaí Norte were not intentional and that the cleared area will not be converted to cropland. Even if the fire events were not intentional for conversion to croplands, they heighten the risk of non-compliance with Nuveen’s zero-deforestation policy and the Brazilian Forest Code, which obliges the restoration of degraded native vegetation on Legal Reserves and Permanent Preservation Areas.

Radar may be linked to land-grabbing in Matopiba

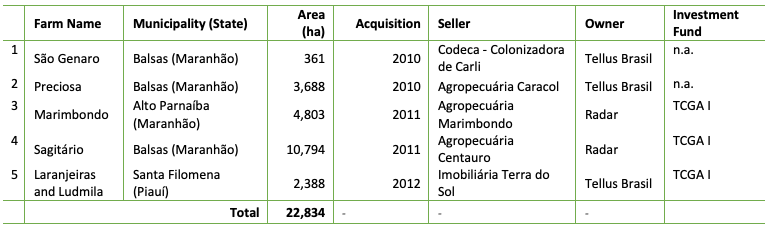

Six farms totaling 22,834 ha within Radar and Tellus properties’ portfolio may be linked to previous land-grabbing crimes in Southern Maranhão. Between 2010 and 2012, Radar and Tellus bought six farms in Southern Maranhão from companies owned by or linked to Euclides de Carli (see Figure 12). De Carli is originally from São José do Rio Preto, São Paulo, but for decades used a business model based on buying, selling or leasing properties in southern Piauí and Maranhão. He is locally known as one of the biggest land-grabbers in the region. In 2016, a local Agrarian Court suspended the titles of properties totaling 6 million ha in Southern Piauí and Maranhão, including 124,000 ha linked to Euclides de Carli. The properties now owned by Radar and Tellus are not among the suspended titles. However, the local Agrarian Court estimates that de Carli is linked to land-grabbing crimes on areas that total 300,000 ha in Maranhão and Piauí. De Carli is also accused of violence and threats connected to invasions of lands occupied by local communities. De Carli died on July 2019 without being convicted in any court cases connected to his land-grabbing. He is still registered as the owner of 16 different companies in Maranhão.

Figure 12: Radar and Tellus properties bought from companies owned by or affiliated with Euclides de Carli

Source: CRR field work October 2019 and Brazilian Tax Office database.

Radar properties are linked to previous social and environmental impacts and direct threats to local communities in Santa Filomena, Piauí. In 2012, Radar acquired the farms Laranjeiras and Ludmila in Santa Filomena, Piauí, from Imobiliária Terra do Sol, owned by Tellus Brasil. The previous owner of the area was Simone de Carli, possibly a relative of Euclides de Carli. The conflicts in the area started in 2010, when de Carli invaded local community’s territory and claimed the title of the area where currently both farms are. In 2015 and 2016, after the farms were bought by Radar, a local community reported that people linked to de Carli set fire to one of the community’s houses near the farms. Environmental impacts are also a concern to local communities. Radar’s Laranjeiras and Ludmila farms are in the highlands or plateaus, and the communities usually live in the low land close by the water sources. Local communities report, however, that the plateaus areas are used for harvesting fruits and herbs and for seasonal animal breeding. As a result, the local communities must contend with a scarcity of water sources; a decrease of water quality due to agrochemicals; health problems caused by the consumption of water from local rivers; impacts on the local fauna (fish); and land degradation. Over the long term, these impacts also threaten food and agricultural production. Radar told CRR that it recognizes some of the externalities highlighted by local communities, but pointed out that its operations in the region bring also some benefits such as employment, infrastructure and small projects that support communities’ development.

Sustainability risks may result in legal, operational and stranded land risks

Radar’s business model of investing in farmland in the Brazilian Matopiba region includes legal, operational and stranded land risks. Sustainability risks in Radar’s business model in Matopiba include deforestation after 2009, recent fire events and potential links to previous land- grabbing cases with impacts on local communities’ livelihood. The exposure of Radar’s business model to these risks may impact TIAA and other investors in the TCGA I and TCGA II funds.

Radar may see legal risks from its potential links to previous land-grabbing cases in the Matopiba region in the Cerrado biome. CRR found at least six farms within Radar’s Matopiba portfolio bought from companies under investigation for being part of one of the largest land-grabbing schemes in the region. These land-grabbing cases are linked to social and environmental impacts that directly affect the livelihood of local communities, possibly exposing Radar to legal risks. In the investigation of these land-grabbing schemes in the Matopiba region, Radar may see fines, legal fees or even to the loss of titles of its properties in the region.

In addition, Radar may face operational risks at farms linked to social and environmental impacts. Social impacts reported by local communities are linked to both Radar’s buying of land and operations of on those lands in the Matopiba region. These social impacts could increase amid demand for new areas as a result of the government’s programme for agribusiness development of Matopiba region, started in 2015, with facilitated loans and credits for crop production in the area. Moreover, demand could also rise because of the after-effects of the 2008 financial crisis, which spurred Brazilian agribusiness to expand its production area. The pressure for opening new production areas, especially in the expansion frontier of Matopiba, has had immediate effects on local communities’ livelihood, including violence, land degradation, water source scarcity and pollution. In the medium to long term, environmental impacts reported by local communities may also compromise large-scale agriculture development in the region.

While the pre-2018 deforestation reported above is not in violation of Nuveen’s zero-deforestation policy, it may nonetheless pose future compensation or stranded land risks. Radar may be held accountable for all land-use changes that took place during the period it held the property. It may not be able to sell properties with post-2009 clearing to any counterparty with a similar or stricter zero-deforestation policy. Acknowledging compensation liability for the equivalent of the 2,970 ha from post-2009 deforestation may help mitigate associated stranded land risks. Recovery or compensation liabilities may also be included in market-access criteria in soft commodity supply chains, as illustrated by recent developments in the Southeast Asian palm oil sector.

Financial risk in Radar’s business model is widespread among various financers

Nuveen, Westchester Group, TIAA, Cosan and financers linked to these entities are exposed to sustainability risks that could become business risks (legal, stranded land and operational risk) as well as reputation risk. Investors and financers linked to Radar’s farmland portfolio are found in various entities:

- Nuveen, the asset manager of TIAA. Several other pension funds have also allocated money to Nuveen’s farmland portfolio. Nuveen has a 97 percent economic stake in Radar’s assets;

-

Cosan is, together with TIAA, the joint shareholder in Radar. Cosan is a listed company with various subsidiaries. Many banks, shareholders and bondholders can be linked to Cosan, which has a 3 percent economic stake in Radar.

The total value loss in Radar’s portfolio could amount to USD 192 million. This calculation is based on the estimate of legal risk (USD 123 million; see below), the value of stranded assets (USD 53 million) and operational risk (USD 16 million). In total, this amount is circa 23 percent of the value of Radar’s assets (USD 830 million; see above). As Nuveen’s real asset portfolio (farmland, timber, infrastructure) is valued at USD 29 billion, the impact of these losses on its portfolio would be 0.6 percent of the total fund. Three percent of USD 224 million would translate into 0.07 percent of the Enterprise Value of Cosan SA on December 18, 2019 (USD 8.8 billion).

Legal risk related to land-grabbing on six farms could cost up to USD 123 million

Radar could be fined for land-grabbing (USD 68 million) and possibly lose land titles (worth USD 55 million), which may impact its enterprise value by USD 123 million. Radar could be fined for land-grabbing and/or lose the land title in six farms with in total 22,834 ha of land (see Figure 13). Agricultural land in Matopiba can be valued at ca BRL 10,000 per hectare, and the loss of this land by Radar would mean a value loss of BRL 228 million (ca USD 55 million).

Although land-grabbing was the result of activity by former owners, Radar could still face fines. The value of the fines could be partly dependent on the numbers of hectares and/or the number of cases. Fines could range between USD 419 per hectare (USD 36 million for 86,000 hectares; one case) to USD 3,000 per hectare for smaller plots (USD 5-9 million per case). Based on the calculation per hectare, fines related to the 22,834 ha on six farms could range from USD 10 million (22,834 ha x 419 per ha) to USD 68 million (22,834 ha x USD 3,000 per ha). The number of fines ordered by the Brazilian government’s environmental agency IBAMA have declined by 29 percent since President Bolsonaro took office.

Stranded land related to the loss of market demand for deforested land valued at USD 53 million

Deforested land could become stranded, possibly affecting Radar’s enterprise value by USD 53 million. Customers may not source from deforested land, which would turn these areas into stranded land. The 2,970-ha deforested land on the six farms in 2009-2018 (Figure 7) plus the land with fires (2,350 ha) total 5,320 ha, putting the value of stranded assets at USD 53 million (based on BRL 10,000 per ha).

Operational risk from community conflicts and water issues could amount to at least USD 16 million

Social conflicts and lack of water could reduce harvests, possibly affecting Radar’s lease revenues and result in a value loss of USD 10 million (DCF-based). The above-mentioned pollution of water resources mainly concerns drinking water for local communities but might also have an impact on the yield of the soybean harvest. CRR estimated in a previous report that yields could decline by up to 40 percent due to drought and evaporation. The Laranjeiras and Ludmila estates have in total 3,188 ha which may be affected by water issues and social conflicts. On average, 3.4 metric tons of soybeans are harvested per ha in Brazil. A 40 percent decline would lead to 1.4 metric tons less per ha and a production decline of 4,463 metric ton in the two estates of 3,188 ha in total. The value of this revenue loss totals USD 1.5 million. As this decline in revenue also means a nearly equal decline in EBITDA, the DCF value could be estimated at USD 10 million. In future negotiations on the lease contracts between landowner Radar and the farmers, these impacts will be considered and could reduce the value of the contracts.

Additionally, social conflicts and violence may lead to high intangible costs of at least USD 6 million, such as the costs associated with violence and the costs from reputation loss. When considering intangible costs in palm oil land conflict, the range was USD 5.6-7.5 million per conflict. These costs will also likely impact the value of the lease contracts.

Cosan’s stake in Radar mainly leads to reputation risk for several financers

Cosan is relatively shielded from changes to its earnings at the three farmland affiliates, although it is officially the majority owner. Against this backdrop, financial risks are relatively low for investors; however, for some of them there could be substantial reputation risk.

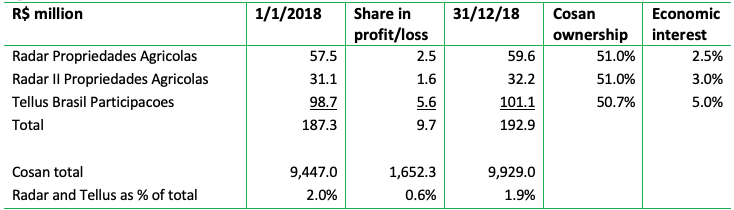

Cosan SA is controlled by Cosan Ltd (62 percent stake), in which Rubens Ometto Silveira Mello has a 16 percent stake. Cosan SA has a 51 percent ownership interest in Radar II Propriedades Agrícolas S.A., and only a three percent economic interest. The same structure accounts for Radar Propriedades Agrícolas S.A. In Tellus Brasil Participações S.A, Cosan also owns a 51 percent interest and a five percent economic interest. Due to the small economic interest, Cosan’s share in the 2018 earnings of the three entities were only respectively BRL 2.5 million, BRL 1.6 million and BRL 5.6 million. As compared to the BRL 1.904 billion earnings of the consolidated Cosan activities, the Radar/Tellus activities contribute only 0.5 percent. In shareholders’ equity of the three entities, Cosan owns approximately BRL 200 million of the total BRL 5 billion total equity.

Figure 13: Consolidated – Cosan – Associate value share

Source: Cosan S.A. Consolidated financial statements as of December 31, 2018

According to Cosan, the three entities saw a total net profit of BRL 250 million in 2018 on total equity of BRL 5 billion. This was a ca 10 percent decline versus 2017.

Concerning debt financing by financial institutions with deforestation policies, in 2014-2019 BNP Paribas financed one of the Cosan entities with USD 125 million (Figure 14). This financing included USD 75 million in a revolving credit facility. BNP Paribas says it is targeting the elimination of upstream and downstream deforestation by 2020. Santander is an even larger financer, with a USD 322 million commitment, of which USD 301 million is in underwriting services, USD 13 million is in revolving credit, and USD 8 million is in loans. Santander has a zero-deforestation policy per 2020. HSBC and Rabobank have smaller exposure but face conflicts with their policies. Rabobank says it does not “accept deforestation, land grabbing or violation of human rights.”

Shareholders of the Cosan entities mainly consist of Brazilian and U.S. shareholders who have no or weak forest policies. But European shareholders Norwegian Government Pension Fund (USD 71 million) and Storebrand (USD 49 million) face conflicts with their policies and may engage.

Several TCGA investors face reputation risk and financial risk

AP2 and Caisse de dépot face reputation risk as the clearing of native vegetation in areas acquired by Radar means that these investors are at high risk of being linked to deforestation. As a result, they would be non-compliant with zero-deforestation policies. From the investor groups mentioned in TCGA I and II, several face conflicts with the (intention of) policies, such as Caisse de dépôt et placement du Québec and Andra AP-Fonden (AP2). AP2 intends to achieve zero-deforestation through Nuveen’s farmland funds. Stichting Pensioenfonds ABP and its asset manager APG have signed the Cerrado Manifesto. Of these three, ABP is only involved in TCGA II, which is confronted with systematic forest fires on one of its farms.

Other large investors in the TCGAs do not have zero-deforestation policies. These include National Pension Service (NPS; South Korea), the New York Common Retirement Fund (CRF; United States) and the New Mexico State Investment Council. British Columbia Investment Management Corporation (BCI) identifies climate change as a priority but does not make explicit mention of deforestation within that context. Finally, Ärzteversorgung Westfalen-Lippe has no ESG policies. Of the smaller TCGA investors, the Environment Agency Pension Fund and Greater Manchester Pension Fund (GMPF) are strongly focused on reducing fossil fuel investments but do not consider deforestation.