The Development Bank of Ethiopia suspending loans for commercial farms because of the failure of numerous farms in Gambella, where the Bank was even tricked into giving two loans for a single agriculture project.

Commercial farms’ domino effect on banks

For a commercial farm investor, who by profession is an agricultural economist, putting his money and energy into commercial farming demonstrates keen interest. Not only was he born into a family of farmers who have been involved in the development of commercial farms but he too has been involved in sectors that are more close to his passion and ambition.

For the past six years he has spent most of his time in Gambella Region. While in the process of accessing the land in Gambella and then after developing the land, many developers would approach the Development Bank of Ethiopia (DBE), the state financier for investments like commercial farms. However, DBE was not on his radar; he rather choose to finance his farm from his pocket.

“Back then it did not even cross my mind to submit a loan application to the Bank,” said the investor whose name is being withheld on request. His exposure to working in a farm equipment supplier company helped him to make his decision. Hearing the frustration of the investor over delayed loans and all sorts of bureaucratic hurdles pushed him to go other way, he said.

There is no consistent manual on how clients can access loans, added the investor. He explained that after an investor secured land, it would take one year to one year and half to secure a loan. Many of the investors submit title deeds for the land and development contracts. Other essential documents such as feasibility studies and bills of quantities are informally done by appropriate bank staff members after paying certain sums of money.

The investor leased 1,000ha of land from the region’s Angyuak Zone.

Unfortunately, he is now among the 100 local investors who were forcibly evicted from their land by the local administration. He, along with other investors were accused of taking land that was reserved by federal government for a special economic zone, though the investors claimed to take the land with full knowledge of regional authorities. Each investor in two weredas, Dimma and Gog, took 500ha to 2,000ha plots of land.

The Region is one of the biggest destinations for investors in large commercial farms because of its large tracts of available land.

“There is no clarity on the loan policy of the Bank,” said the investor.

To make matters worse, three weeks ago, DBE ceased to extend loans for commercial farms.

Being the sole financier did not stop the bank from discontinuing loan disbursements for the agricultural sector. The rationale for the change in policy was to restructure the way the Bank has been performing as far as loans and loan disbursement are concerned. The Bank issued circular stating that it was suspending loans for commercial farms for an undetermined period of time.

An issue that led to this decision was the extent of failure in commercial farms in Gambella where the Bank was even tricked into giving two loans for a single agriculture project.

Data from the DBE indicate that the bank has registered double digits in non-performing loans from its total loan disbursement. Though the Bank targeted keeping these at 11.05pc, they escalated to 17.35pc.

However, experts close to the operations of the Bank indicate that the textiles and apparel industry accounted for up to 60pc of bad loans in the past six months. Yet it continues to grant loans to this sector.

Though the intrinsic paradox stands out, the expert said the decision to suspend extending loans is rather a policy direction where decision makers from related sectors came together and agree.

The first blink of official admission of serious problem with the sector was noted when the Agricultural Investment Land Administration Agency (AILAA) bombarded the sector with a tough decision. The Agency is a body mandated to allocate lands above 5,000ha and at the same time to follow up the activities of foreign investors. In December last year, the Agency took measures against 18 large commercial farm investments owned by both local and foreign developers, that had performed far below expectation.

There are 97 large scale agricultural investors licensed by the Agency at the Federal level. A total of 2.43 million hectares of land is under the control of local investors, while 476,000ha was allowed to the 97 big investors. Another 5,583ha was allocated to the others bringing the total area of land to 1.94 million hectares.

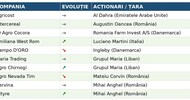

The latest measures on failed projects range from first warning, to termination of lease rights over the land they took. Developers occupied 215,000ha of land with an Indian company, Karaturi Agro Product Plc, having the lion’s share with 100,000ha of land. This company along with a second investor, called BHO Bio Product Plc faced a final farewell. From the total 197,000ha of land was taken from Gambella Region.

Karaturi is fighting the decision by CBE to foreclose but BHO has kept quiet.

Despite its rebuttal against termination, CBE is not backing down. The matter has reached to court. It must be noted though, that not everyone who received warning signals and the red card from the Agency ends up in trouble with lenders because they have continued to make their loan repayments on time.

This was not the case with White Field Cotton Farm Plc, an Indian company among the 18 investments. It leased 10,000ha of land at Southern Regional State, South Omo Zone, Dasenche Wereda in 2010 from the Agency. Back then it agreed to make annual payments of 1.58 million Br with a total payment of 39.5 million Br. It was granted a grace period of three years.

The land was leased for 25 years. However given the poor performance, its fate was sealed with the warning letter.

Surprisingly, prior to the warning from the Agency, DBE had auctioned the property owned by the company in return for the loan it gave for project financing. The initial bidding price quoted during the bid announcement in Addis Zemen newspaper on October 24, 2015 was 35.1 million Br.

This and similar cases have resulted a hike in the non performing loans as reported by the Bank.

DBE incurred a 100pc increase in its non-performing loans portfolio to the tune of 3.4 billion Br in 2014/15. The official report of the Bank attributed the increment to prolonged unpaid loans and agricultural production failures mainly by large scale commercial farms as a cause.

“It is not just the investor who failed, it is the Bank!” the investor exclaimed.

After all it is the bank that approves the feasibility studies of the projects, to follow the progress of their investment.

It is not just DBE that feels the burnt. Other cases indicate that there is a correlation between loan disbursements and higher NPL’s. Banks having higher disbursements to agricultural projects also had a higher NPL ranking. Zemen Bank with 12.04pc in loan disbursement reported a 5.53pc provision for bad debt, while Abay Bank with 4.12pc of loans also recoded 3.44pc of provision.

The reverse trend is true for Awash Bank with a low proportion of loans for agriculture and NPL provision of 0.25pc.

To the contrary, Bank of Abyssinia (BoA) loans are high, despite more foreclosures. BoA has successively increased loans disbursed to agriculture from 2014 to the current fiscal year. In 2014 agricultural loans totaled 15.2 million Br; one these increased to 37.8 million Br. For this half fiscal year total loans had quadrupled to 117 million Br. However this has also come with its own risks. Two years ago the non performing loans which means loans that have not been paid for more than three months, was 15 million Br. This figure has most significantly hiked to 21.8 million Br for the current half financial year.

“The sector is highly dependent on externalities,” said Daniel G Medhin, BoA’s director for Credit Appraisal, Review & Portfolio Department. He attributed the low performance of loan disbursement to agriculture to this factor.

The NPL for this year increased because of failed investment in sesame farms as the result of a decline in price of sesame on the international market.

“We focus less on agriculture but even if we do, we give loans for our customers that export their products with anticipation that we get the hard currency,” said Daniel.

Once we have the collateral we give the loan at once, he said. No technical assistance will be offered to the client.

Though not incomparable with other sectors, loan financing is still available to the sector but many prove to be high risk loans with defaulted payments. In its half year report the Commercial Bank of Ethiopia (CBE) has witnessed a raise in the number of projects that went to foreclosure. Last year it was only about two commercial farm investments which both amounted to 55 million Br. The current half year however has received three farms so far with a total cost of 68 million Br.

There are also three development projects that are expected to be announced for foreclosure.

Looking at its non-performing loan ratio: in 2012/13 it was 2.2pc, in 2013/14 it went down to 1.4pc and last year it increased to 1.8pc.

In 2014/15 total number of loans issued amounted to 265 billion Br.

The situation in the private banks may be contrasted as their loan portfolio for agriculture is low in comparison to other sector. Yet, the way loans are disbursed, reveal their own gaps.

In 2015, private banks disbursed 75.5 billion Br in total loans of which only 1.24pc went to the agri sector in contrast with the manufacturing sector which took 12.8pc, almost ten times higher.

Large scale agriculture farming is suffering due to infrastructure, regulation overlap between federal and regional authorities. This in return affected the banks’ operations.

Throughout the current half fiscal year, both public and private banks announced 18 auctions in just agriculture investments. Of total auctions, the share of private banks is 7.3 million Br while the rest 72.1 million (91pc) issued by the two state-owned banks.

The CEO of one long-established private bank shared Daniel’s argument.

“I don’t think private banks have either the interest or active engagement in the sector,” he said. “We often give loan in search of hard currency from their export and to customer that may have influence in other sectors.”

Private banks have no dedicated structure that will manage the loans they disbursd to the sector, nor do they have experts trained in the sector.

“Banks don’t dare to give loans in agriculture,” said Haddisu Haba, president of Debub Global Bank. His bank has decreased loans to agriculture by 50pc from 2014 to 2015.

For Taye Debekulu of United Bank one reason for banks to stray away from the sector is that there is no dedicated insurance company that could support banks to mitigate their risk.

An agricultural expert and a lecturer at Haromaya University is of the view that failure of commercial agricultural investment is due to the insignificant land lease price the investor has to pay.

Of34 commercial farms given to developers from 2001 to 2012 the minimum lease price was 20 Br for a square metre of land.

The fact that the lease price required is the minimum, developers are not that much concerned to have the return. Again he argues that not everyone with money should not be allowed to have its hand in the sector.

There should at least be familiarity with agricultural practice on a large scale, said the expert whose name is being withheld on his request.

He suggested a change in the land policy where anyone can sell and buy it at a market price so the price will be determined by market forces.

A high level task force that comprises the Ministry of Agriculture & Natural Resources, the Agency, and the state-owned banks are assessing the problem to come up with a lasting solution.

However, both the investor and the expert criticized the task-force for non inclusion of the investors.

“No one has so far approached us from the task force,” said the same investor.