Jaguar Pension Plan of the UK opts for forestry and farmland

Pensions Expert | 5 November 2018

Jaguar scheme opts for forestry and farmland

By Alex Janiaud

The Jaguar Pension Plan has invested in agriculture and timber funds in a bid to diversify its portfolio and develop its exposure to opportunistic private markets.

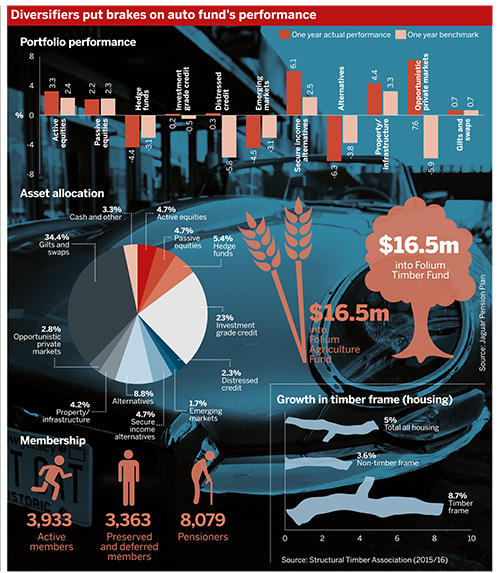

According to its latest investment report, the £3.7bn scheme invested $16.5m (£12.3m) in an agriculture fund managed by Boston-based specialist Folium Capital in the year to April 5 2018.

It invested the same amount in a timber fund run by the same asset manager.

However, the Jaguar scheme has blamed diversification for recent underperformance. Losses from “diversifying assets, hedge funds and emerging markets” mean the fund lagged expectations, according to its accounts, which did not disclose the portfolio’s performance as of April 5. It said its performance over the year was led by investments in real estate and infrastructure.

Experts praise agriculture and timber investment for their diversifying benefits and inflation linkage, but say the governance burden of these investments and a small market largely restrict them to bigger funds.

A spokesperson from Jaguar declined to comment.

Specialist markets require strong governance

Research by consultancy Mercer indicates that in 2018, 2 per cent of European pension schemes held part of their exposure to real assets in timberland or agriculture.

Of these schemes, the average asset allocation stood at 2 per cent. The Jaguar plan sits in a range of large UK schemes with exposure to agriculture and timber.

The circa £30bn Pension Protection Fund’s 22.5 per cent strategic allocation for alternatives includes investment in farmland and timberland, according to its website.

The £6.6bn Lothian Pension Fund, meanwhile, holds a 1.7 per cent allocation towards timber that is managed in-house.

Timber funds invest largely in freehold land, according to Edward Daniels, a director in real asset investment manager FIM’s forestry team.

Some investors own the right to the timber, as well as the land underneath it. Alternatively, they may just own the rights to the crop.

Meanwhile, agriculture funds invest in land and subsequently farm it to provide income, Daniels said.

“It’s a very niche market,” he said. The main investment driver for forestry investment is the global timber price, he noted.

The proportion of UK houses relying on a timber frame as a building system grew by 8.7 per cent over 2015/16 in volume terms, compared to a 3.6 per cent growth of those made with non-timber frames, according to the Structural Timber Association.

“From 2009 onwards we have been increasingly consuming more and more timber globally and we expect... that to continue into the future,” Daniels said.

America first in timber markets

According to reports, Folium Capital is run by former managers of the Harvard Management Company, which operates Harvard University’s $37.1bn endowment fund.

Daniels said that agriculture and timber both offer sources of diversification for a scheme portfolio.

Linda McAleer, an investment research consultant at Hymans Robertson who specialises in real assets, agreed, adding that the investments should also offer Jaguar inflation protection and will provide the scheme with access to long-term income.

Timberland has received more institutional investment than agriculture because of the “fragmented nature of the agriculture market”, according to McAleer.

“It is mostly larger schemes that access these asset classes,” she added, “and that’s predominantly because of the governance burden”.

Australasia and South America are two key markets for these investments. Timberland and agriculture are, however, “very US-centric”, McAleer said.

Hugh Nolan, director at Spence & Partners, said that the investments are “not a massive gamble by any means”, and that adopting an innovative approach to selecting asset classes is sensible at a time of heightened market uncertainty.

“There are some difficulties in markets at the moment in terms of trying to work out where the best returns are coming from,” he said.

Infrastructure becoming more liquid

The Jaguar plan’s investment report states: “Investment performance over the year was driven by investments in real estate and infrastructure-related investments.”

Interest in real estate has been relatively consistent across UK schemes, according to research by UBS Asset Management.

In the first quarter of 2016, the average scheme exposure to real estate stood at 8 per cent. It has dipped no lower than 6 per cent since 2001.

Simeon Willis, chief investment officer at XPS Pensions, holds some concerns over real estate. Brexit uncertainty is particularly worrying for the prospects of UK property, he said.

Willis observed that retail real estate has had to contend with a challenging environment, but “the less glamorous locations have fared better”, such as industrial units and out-of-town manufacturing.

He recognised that infrastructure has proven very popular in recent times, with a proliferation of infrastructure products coming to market.

A lack of liquidity is a risk factor that accompanies alternative assets such as timber and agriculture, along with the more conventional alternative assets.

Willis noted that some managers in the infrastructure space are taking steps to address this worry. “Some of the newer open-ended funds,” he said, offer schemes the opportunity to “go in and come out at your own choosing, rather than entering into a closed fund that lasts for, say, 10 years and then boots you out”.

End of QE could help active management

Jaguar’s latest investment report largely attributes the underperformance of its diversifying assets, hedge funds and emerging markets exposure to low market volatility and the effects of quantitative easing.

Low volatility reduced “the opportunity for active managers to add value”, the accounts read.

The CBOE Volatility Index, or Vix, which measures the expected volatility of the US stock market, closed at 19.8 on April 5 2018.

Barring a momentary spike in February, the Vix varied little in the 12 months leading to April.

Phil Organ, associate director at Leodis Wealth, observed that the Jaguar plan’s asset allocation is “far from the ‘traditional’ client portfolio where low volatility and quantitative easing helped drive good returns”.

Jaguar’s scheme holds a relatively small proportion of its portfolio in equities, the value of which some experts view as having been propped up by QE. It has 4.7 per cent invested in active equities and another 4.7 per cent in passive equities.

It has a substantial asset manager roster, with 11 managers alone covering opportunistic private markets.

“Low market volatility will have been challenging for diversifying (non-equity) strategies as many trade on volatility in order to benefit from market anomalies – these anomalies are few and far between when volatility is low,” he said.

Ross Leach, co-head at River and Mercantile Solutions, said that QE boosted developed market equities, with US equities performing particularly strongly, “and emerging markets to an extent got left behind”.

The European Central Bank plans to end its bond-buying programme in December 2018. The US Federal Reserve raised interest rates in September to 2.25 per cent. A period of quantitative tightening looks set to ensue.

“Going forward, if we start to see quantitative easing start to unwind… a return to some sort of assessment of fundamental value might well be open,” he said.

“Whether that’s active management, whether that’s relative value strategies, they probably have more scope to generate performance going forward.”